- Acumen Powered by Robins Kaplan LLP®

- Affirmative Recovery

- American Indian Law and Policy

- Antitrust and Trade Regulation

- Appellate Advocacy and Guidance

- Business Litigation

- Civil Rights and Police Misconduct

- Class Action Litigation

- Commercial/Project Finance and Real Estate

- Corporate Governance and Special Situations

- Corporate Restructuring and Bankruptcy

- Domestic and International Arbitration

- Entertainment and Media Litigation

- Health Care Litigation

- Insurance and Catastrophic Loss

- Intellectual Property and Technology Litigation

- Mass Tort Attorneys

- Medical Malpractice Attorneys

- Personal Injury Attorneys

- Telecommunications Litigation and Arbitration

- Wealth Planning, Administration, and Fiduciary Disputes

Acumen Powered by Robins Kaplan LLP®

Ediscovery, Applied Science and Economics, and Litigation Support Solutions

-

April 23, 2024David Martinez Recognized Among Top 100 Lawyers in Los Angeles by LA Business Journal

-

April 15, 2024Robins Kaplan Named to 2024 BTI Client Service A-Team

-

April 9, 2024Robins Kaplan LLP Files Complaint Against Social Media Giants Meta, Snap, TikTok on Behalf of Spirit Lake Nation, Menominee Indian Tribe of Wisconsin

-

April 30, 2024Navigating Generational Dynamics

-

May 2-3, 2024ACI Advanced Forum on Managed Care Disputes and Litigation

-

May 6, 2024Litigating with the Legends

-

First QuarterGENERICally Speaking: A Hatch-Waxman Litigation Bulletin

-

March 2024e-Commerce: Pitfalls and Protections

-

March 25, 2024Endo Ventures Unlimited Co. v. Nexus Pharms. Inc.

-

September 16, 2022Uber Company Systems Compromised by Widespread Cyber Hack

-

September 15, 2022US Averts Rail Workers Strike With Last-Minute Tentative Deal

-

September 14, 2022Hotter-Than-Expected August Inflation Prompts Massive Wall Street Selloff

Find additional firm contact information for press inquiries.

Find resources to help navigate legal and business complexities.

I’ve Reached My Limit: Exploring the Fire Damage Legal Liability Limit in Commercial General Liability Policies

Discussing the application of legal liability limits to varying types of tenancies.

April 22, 2019

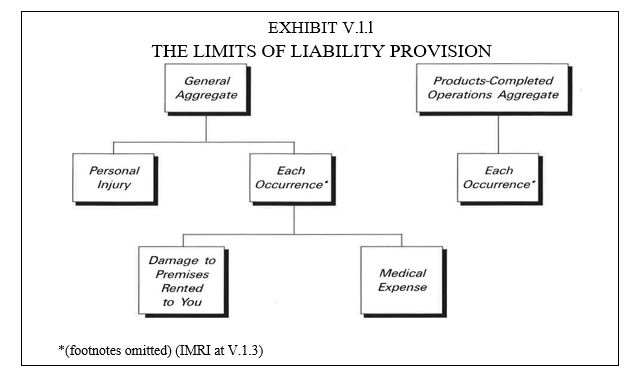

In the face of a fire that results in damage to multiple units of a commercial building, it can be difficult for insurers to determine the scope and extent of coverage available under a commercial general liability policy. Indeed, one must think critically about how the policy limits will interact, particularly where the claim involves property damage, damage to contents, and different types of tenancies.

Under the “fire damage legal liability” exception to the exclusions contained in Coverage A of the current standard commercial general liability (“CGL”) ISO policy, coverage is added back for fire damage sustained to a premises rented to a covered insured where that damage was caused by an insured’s negligence.1 This coverage is subject to a separate sublimit titled “Damage to Premises Rented to You,” which “establishes the maximum that will be paid for loss arising out of any one fire that is covered as a result of the fire damage exception [. . . ].”2 Both the coverage grant and the limits of liability extend to property damage only. Damage to contents is not included under this sublimit, but may be available under the general aggregate limit.3

As outlined in the table below, a covered fire loss to a rented premises remains subject to the policy’s per occurrence limit and/or general aggregate limit.4 Once the insured reaches the sublimit for the rented space, it must look to the each-occurrence limit or the general aggregate limit to recover for any additional property damage to the non-rented space, if any. The insured cannot recover in excess of the “Damage to Premises Rented to You” sublimit for property damage to the rented space.5 What may be available under the policy for the non-rented space is determined by subtracting the amount paid for the rented space under the “Damage to Premises Rented to You” sublimit from the per-occurrence and/or general aggregate policy limit.6

Application of limits can become more complex. For example, consider a claim involving fire-damaged units leased to both (1) individual tenants, and (2) social services organizations who then sublease the units to individuals in need of housing. Claims involving “property damage” due to fire caused by the negligence of a tenant placed by a social services organization may trigger yet another sublimit specific to this particular style of tenancy which is likely to be included by way of endorsement. The “Damage to Premises Rented to You” limit is instructive to how limits may apply in that type of scenario.

Any additional sublimit is likely to encompass only the “property damage” caused by the placed-tenant and to the unit sublet specifically to that tenant. In other words, where a claim involves damage to (1) units sublet to placed-tenants and (2) to units leased to individual tenants, the property damage sustained to the space sublet to the placed-tenants is likely to be subject to a separate sublimit, while the property damage sustained to the space leased by individual tenants would be subject to the remaining per occurrence or aggregate limit.

As fire legal liability policy language continues to evolve to address more complex tenancies, the application of limits will require one to consider more and more coverage questions. The general principles set forth above may assist those navigating the increasingly complex world of fire damage legal liability claims.

1 See Woodward et al, “Commercial Liability Insurance” at V.D.230-31 (International Risk Management Institute, Inc., Vol. I, 2010) [hereinafter, “IRMI”]. The fire damage legal liability coverage enhancement, together with the sublimit, was clarified in the broad form comprehensive general liability endorsement in 1976 and again in 1986. Id. at IV.D.3 to IV.E.5. Many other coverage issues may be triggered in making this determination. Note that under the ISO form, coverage applies only if the insured is legally liable for the fire damage because of negligence; the contractual liability exclusion is not affected by this provision. Id. at V.D.230-31.

2 20-129 Appleman on Insurance Law & Practice Archive § 129.2 (2nd 2011); IRMI at V.D.230 (Nov. 2013); IRMI at V.1.5 (Aug. 2008).

3 Mutual of Enumclaw Ins. Co. v. Ensign Traders, LLC et al., No. 2:13-cv-00865-DN, 2015 U.S. Dist. LEXIS 38773, at *6-7, 10-12 (D. Utah Mar. 26, 2015); Safway Services, LLC v. Anthony Filo Construction, Inc., No. CV 12 781207, 2013 Ohio Misc. LEXIS 73 (Ohio Com. Pl. Cuyahoga Cnty. Dec. 26, 2013).

4 IRMI at IV.E.14-15. The per-occurrence limit of liability for property damage was established in earlier versions (1973 and 1986) of the ISO form. Originally, the fire damage sublimit was subject to the per-occurrence limit, but not the general aggregate limit. Id. Depending on the language contained in the policy at issue, the “Damage to Premises Rented to You” may be subject to both limits.

5 IRMI at V.I.3 (Aug. 2008).

6 “General Provisions of the CGL,” The American Lawyer (Online) (Nov. 4, 2013); IRMI at IV.E.14-15 (Oct. 1996) (“The general aggregate limit [. . .] can also work to reduce the each occurrence limit if these aggregates have been reduced to an amount lower than the occurrence limit because of earlier payments”).

Related Professionals

Taylore Karpa Schollard

Associate

Related Publications

Related News

If you are interested in having us represent you, you should call us so we can determine whether the matter is one for which we are willing or able to accept professional responsibility. We will not make this determination by e-mail communication. The telephone numbers and addresses for our offices are listed on this page. We reserve the right to decline any representation. We may be required to decline representation if it would create a conflict of interest with our other clients.

By accepting these terms, you are confirming that you have read and understood this important notice.