- Acumen Powered by Robins Kaplan LLP®

- Affirmative Recovery

- American Indian Law and Policy

- Antitrust and Trade Regulation

- Appellate Advocacy and Guidance

- Business Litigation

- Civil Rights and Police Misconduct

- Class Action Litigation

- Commercial/Project Finance and Real Estate

- Corporate Governance and Special Situations

- Corporate Restructuring and Bankruptcy

- Domestic and International Arbitration

- Entertainment and Media Litigation

- Health Care Litigation

- Insurance and Catastrophic Loss

- Intellectual Property and Technology Litigation

- Mass Tort Attorneys

- Medical Malpractice Attorneys

- Personal Injury Attorneys

- Telecommunications Litigation and Arbitration

- Wealth Planning, Administration, and Fiduciary Disputes

Acumen Powered by Robins Kaplan LLP®

Ediscovery, Applied Science and Economics, and Litigation Support Solutions

-

April 15, 2024Robins Kaplan Named to 2024 BTI Client Service A-Team

-

April 9, 2024Robins Kaplan LLP Files Complaint Against Social Media Giants Meta, Snap, TikTok on Behalf of Spirit Lake Nation, Menominee Indian Tribe of Wisconsin

-

April 8, 2024Tara Sutton, Emily Tremblay Shortlisted for Euromoney’s Women in Business Law Awards

-

April 24, 2024IP Leadership Executive Summit

-

April 24, 2024IP Odyssey: Navigating the Latest Developments in Intellectual Property Law

-

April 30, 2024Navigating Generational Dynamics

-

March 2024e-Commerce: Pitfalls and Protections

-

March 22, 2024‘In re Cellect’:

-

March 14, 2024How Many Cases Have You Tried to a Verdict?

-

September 16, 2022Uber Company Systems Compromised by Widespread Cyber Hack

-

September 15, 2022US Averts Rail Workers Strike With Last-Minute Tentative Deal

-

September 14, 2022Hotter-Than-Expected August Inflation Prompts Massive Wall Street Selloff

Find additional firm contact information for press inquiries.

Find resources to help navigate legal and business complexities.

Leveraged Products For Retail Investors Pose Hidden Risks

December 10, 2017

Commodity-related investments have enjoyed a distinct focus from issuers and purchasers of ETPs due to their ease of use and tax-friendly features. Volatile asset classes, combined with leverage, have proven alluring to many wishing to achieve a high return quickly. Because of the potential for these products to be misused, however, the SEC has issued a warning that “individual investors may be confused about the performance objectives of leveraged and inverse ETFs.”

The SEC, FINRA, and brokerages have taken steps to protect individual investors against a variety of products. For example, when investors trade commodities or use margin, professionals review applications which analyze the sophistication of the investor and their ability to manage and understand risk. These factors generally mean that commodities are off limits to a retail investor. Although some ETPs present equivalent complications and risks, there are no similar safeguards or applications for ETPs covering the same market segments.

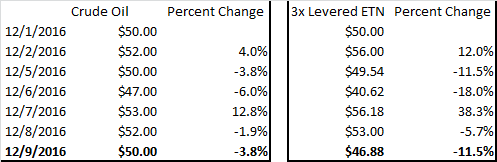

Leveraged ETPs can be especially complicated. To an ordinary person, a fund that advertises returns at three times a benchmark may sound like a great investment. What these retail investors may not realize, however, is that these funds only guarantee a daily performance of three times the benchmark. Each day, the product rebalances and adjusts its leverage accordingly. This mechanism means that, over time, returns will diverge from the expected value. This daily compounding and rebalancing causes decay. Consider the following hypothetical price actions:

Holding the products for more than one day can cause decay, inducing investment loss even if the underlying asset increases in value or maintains the same value.

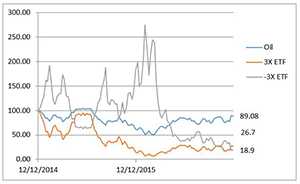

While oil lost nearly 10% during this two-year period, the inverse ETP lost more than 80% of its value despite its inverse relation. Oddly, the inverse ETP actually performs worse than the non-inverse product, despite the decrease in the asset it seeks to track.

For retail investors who are not sophisticated, the disclosures may be inadequate to inform or dissuade them on purchasing speculative products. The nuances in the construction of leveraged ETPs, underlying indexes and assets, and leveraged decay, create products retail investors may not truly understand. Even financial advisors have misunderstood these products. FINRA fined Wells Fargo on October 16, 2017, for recommending the products as a long-term hold to some customers. Despite their risks and complications, these products are both readily available and heavily marketed to uninformed retail investors. Distributors and issuers of leveraged ETPs cast a wide net to promote these products—often catching retail investors.

Distributors and issuers often claim that the intended buyers of ETPs are institutional investors. However, institutional investors have access to products superior to levered ETPs. From 2014 through 2016, institutional investors seldom accounted for more than 50% of the holdings of a formerly-popular ETN, UWTI; and usually accounted for less than 5%. Data further indicates that many unsophisticated investors misuse ETPs, holding them on average for three days—inviting losses due to decay. Finally, the largest holders of such products are the popular retail brokers, such as Charles Schwab, TD Ameritrade, and E*Trade; and these brokers tend to account for a majority of the holders of leveraged ETPs.

In December 2016 Credit Suisse delisted its hugely popular 3x and -3x oil ETNs. The closure of popular and lucrative exchange-traded products, like the two they delisted, is curious. In fact, UWTI has the dubious privilege of being the first ETP to close with more than $1 billion in assets. During the life of UWTI, Credit Suisse received about $2 billion more in proceeds from issuing notes than it had to pay in redemptions. They were essentially being paid to issue this interest-free debt, and then didn’t have to repay it; as the value of the debt they issued was significantly reduced by leverage decay. A product that prints money is rare, so it certainly had to generate great concern within Credit Suisse for them to kill the product. The closure of a winner may indicate Credit Suisse’s ultimate view of the product type. Regardless, after the delisting announcement, only one day passed until a different bank offered a nearly identical product.

Institutional, sophisticated investors are able to access leverage with ease: rendering these ETPs of little use to them. Their existence only functions as a way of allowing retail investors to participate in the use of leverage without having to muster basic margin requirements. The SEC should consider prohibiting both leveraged ETPs and commodities-based ETPs. Investors who still wish to access similar products would still be able to, upon their completion and acceptance of applications and appropriate maintenance of their accounts. While these products can provide short-term gains, their structures and availability mean that investors often end up with more than they bargained for—and less money than they started with.

© 2017 Seeking Alpha

The articles on our website include some of the publications and papers authored by our attorneys, both before and after they joined our firm. The content of these articles should not be taken as legal advice. The views and opinions expressed in this article are those of the author(s) and do not necessarily reflect the views or official position of Robins Kaplan LLP.

Related Professionals

Related Publications

Related News

If you are interested in having us represent you, you should call us so we can determine whether the matter is one for which we are willing or able to accept professional responsibility. We will not make this determination by e-mail communication. The telephone numbers and addresses for our offices are listed on this page. We reserve the right to decline any representation. We may be required to decline representation if it would create a conflict of interest with our other clients.

By accepting these terms, you are confirming that you have read and understood this important notice.